Did you know that even the corporate world has been moving towards a more sustainable approach for some years?

I am Sara, a consultant for the tourism sector, and on this site, I talk about tourism, sustainability, theory and practical ways to become a more sustainable operator.

Before you continue, subscribe to the newsletter if these topics interest you! So you won’t miss a single update.

Today’s topics

– CSR: corporate social responsibility introduction and considerations;

– From ethical principles to ESG (Environment, Social, Governance) model;

– Social and Environmental Reporting.

Through years of studying, working and understanding sustainability in tourism, I have realised how important it is to have benchmarks and guidelines that can help businesses of all levels find ways to achieve their sustainability goals.

This need led me to expand my horizons at first in the international sense of the criteria for the sector. So I studied and understood the GSTC criteria. The GSTC council is an international organisation of the tourism sector that provides the basis for assessing whether the sector’s certifications meet minimum standards and promote a truly sustainable approach to tourism.

A few weeks ago, I approached, so far from a theoretical point of view, the corporate world. I have come across topics I have already seen (such as GRI standards) and have been able to delve into corporate social responsibility. I chose this direction because I believe it is one of the best ways to go against greenwashing and have a few more tools to evaluate larger companies and their strategies.

My primary source of information is Italia and is the book Communicating Sustainability, Beyond Greenwashing by Professor Aldo Bolognini Cobianchi.

Corporate Social Responsibility definition and considerations

Corporate Social Responsibility concerns ethical implications within the strategic business vision in economic and financial terminology. It is a manifestation of the willingness of large, small and medium-sized enterprises to manage social and ethical impact issues within their business effectively and in their areas of activity.

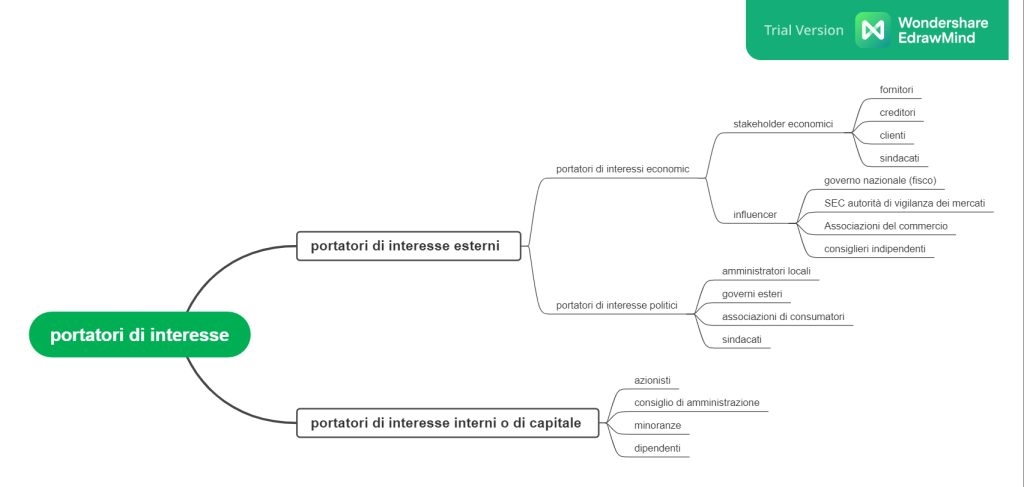

The behaviour demanded of the company is what is known as socially responsible. It is considered not only the legal responsibility of the company but a responsibility that involves vast swathes of subjects who, although they are not owners of shares, have a de facto interest in participating in the management of the company itself (the so-called stakeholders).

Corporate social responsibility can be said to involve two different dimensions: the internal dimension within the company, i.e. the attention that must be paid to its human resources, and the external dimension, i.e. the attention paid to the outside world, i.e. the relationship with the local community, business partners, consumers, suppliers and the environment in general.

Regarding the first aspect, CSR requires that the company guarantees fair pay and career opportunities for women and men (without discrimination), the hiring of disadvantaged groups, the possibility of training staff throughout their working careers, and finally, an essential element, safety in the workplace.

The relationship with the rest of the world lies in guaranteeing respect for the environment in which it operates. Therefore, the company should favour where it conducts its activities by developing local professionalism and protecting the environment (reducing the polluting impact).

Altogether, the people involved forming the set of stakeholders.

The relationship with stakeholders is mainly based on ethical grounds, i.e. on moral obligations, the company imposes on itself to meet their legitimate expectations.

There is (as yet) no law that requires the expectations of all the different categories of stakeholders to be met, although some of these are regulated by law: for example, the obligation to compensate shareholders, to pay employees and collaborators, to pay suppliers, to give customers products that conform to the promised characteristics, to pay taxes to the state and local authorities, and so on.

Ethical codes, ESG model and sustainability reports

Other obligations derive from contractual clauses. But, in general, what governs the whole matter are the moral obligations to which the company agrees to submit to be responsible and thus sustainable.

But where are these ethical bases written down? They are usually laid down in policy documents called codes of ethics.

In these codes, the company or organisation that draws them up describes everything it undertakes to do (or not to do) about the different categories of stakeholders.

Codes are not binding; they are voluntary, non-binding, or soft law. Nobody obliges companies or organisations to follow what is stated. In addition, there are no tools to measure their actual application objectively.

On the other hand, there are forms of certification of the application of different soft law standards (such as ISO standards), i.e. internal company rules that can be imposed as contractual clauses. One example is firing an employee who does not comply with the ethical regulations expressed in the employment contract or terminating relations with suppliers who do not comply with the ethical standards set by the company, provided that these are made explicit in the supply contracts.

There are also criteria for ethical standards that apply to everyone because the market has given itself criteria. These criteria are called ESG and cover three factors: environment, social (responsibility), and governance, the three criteria on which sustainability is based. The ESG criteria originated in the financial market to allow investors to define the degree of sustainability of a company or security. The criteria originated in the 1970s and 1980s. Since 2008, they have become firmly established to replace the previous standards that determined the decision to invest in security, which was undermined by the crisis.

There is only one historical difference between environmental, social and sustainability reporting.

The environmental report was born first in the 1980s. It was absorbed by the social report in the 1990s and was supplanted by the sustainability report in the mid-2000s.

Currently, only non-profit companies and cooperatives continue to produce social reports due to these types of companies’ more humanitarian and solidarity-oriented direction. However, among non-profit organisations, third sector entities (ETS) are obliged to have a social report if they exceed certain size thresholds.

Organisations and international initiatives for corporate social responsibility

On a supranational and global level, the initiative most worthy of mention is the UN Global Compact.

This is a network of national and international organisations from the world’s regions, recommended by the UN Secretary-General in Davos in 1999.

The network aims at the realisation of two objectives: the first is related to the willingness of the company to integrate the principles of the Global Compact into its internal structure; the second is to involve different stakeholders in the cooperation and resolution of rather significant issues. The overall goal is to be able to create a ‘more sustainable and inclusive market.

The principles that the Global Compact recognises as indispensable are:

- Human Rights

- Labour

- Environment

- Fight against corruption.

The first initiative the OECD took on this subject dates back to 1976 when the Guidelines for Multinational Enterprises were first adopted. However, this document has gained more relevance recently, as it was revised in 2000, making it more relevant to the issues affecting enterprises and their socially responsible management.

According to the European Union, a socially responsible company aims to meet the customer’s needs and contribute to society’s needs.

In 2001 the European Commission published a document, the so-called Green Paper, “Promoting a European Framework for Corporate Social Responsibility”, on corporate social responsibility as a form of support for all companies.

It followed the work of the Lisbon Conference in 2000, where the new European Employment Strategy was defined and promoted for the first time.

This document resulted in the Communication on ‘Corporate Social Responsibility: A business contribution to Sustainable Development. It proposes a balanced strategy to develop different CSR instruments, including integrating corporate social responsibility into all EU policies.

The implementation in Italy of strategies to integrate the concepts of Corporate Social Responsibility is mainly left to the government, particularly the Ministry of Labour, which has set up a Multi-stakeholder Forum.

The objectives that the Ministry proposes to achieve are:

- to develop those practices that favour the dissemination of the CSR culture;

- that enable the evaluation of the performance of companies in this area;

- and that aims to support SMEs, representing our entrepreneurial system’s substratum.

The realisation of these objectives is also supported by encouraging the exchange of experiences with other countries to be able to apply the best practices already found internationally.

The ‘CSR Forum‘ (Italian Multi-Stakeholder Forum for Corporate Social Responsibility) was established, which aims precisely to put government intentions into practice through a series of initiatives to raise awareness of the importance of the relationship between CSR and sustainable development.

Sources

- Comunicare la sostenibilità, oltre il green washing. Aldo Bolognini Cobianchi.

- https://sustainabilityaward.it/che-cosa-e-la-responsabilita-sociale-dimpresa/;

- https://www.fondazionenazionalecommercialisti.it/system/files/imce/aree-tematiche/pac/ET_RSI_%20ETICA.pdf;

- https://coopthc.org/la-responsabilita-sociale-dimpresa-cose-principi-e-vantaggi/;

- https://www.contributipmi.it/responsabilita-sociale-di-impresa/

Sara – tourism sector consultant